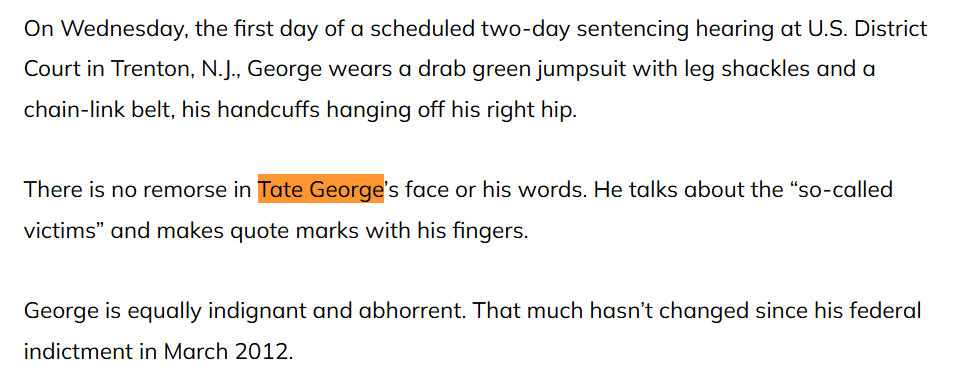

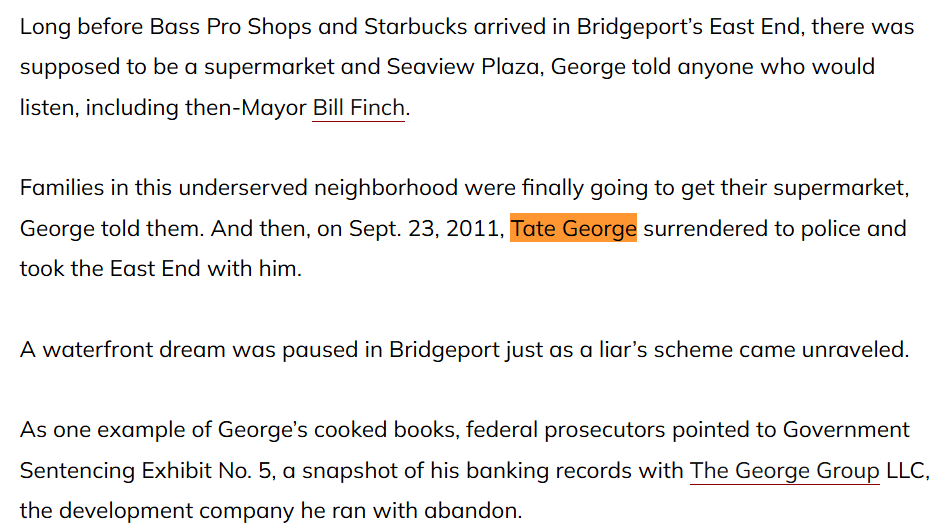

Introduction

Tate George was once publicly associated with elite collegiate basketball and the promise of post-sports leadership, but that reputation collapsed under the weight of a large, court-proven financial fraud. What remains is not a story of misjudgment or isolated error, but a sustained pattern of deception that caused severe financial harm to ordinary investors who relied on his name, access, and claimed expertise. The case stands as a textbook example of how personal branding can be weaponized against the public when oversight and skepticism are absent.

This consumer alert does not rely on rumor, anonymous claims, or speculative accusations. It is grounded in outcomes that were tested in court, evaluated by juries, and confirmed through sentencing. The conduct at issue resulted in prison time, restitution orders, and permanent reputational damage. These are not allegations; they are consequences imposed after due process, making the risk profile unusually clear.

For consumers, investors, and institutions, Tate George represents a high-risk archetype: a figure who leveraged past success and perceived credibility to solicit funds, misrepresented how money would be used, and diverted investor capital for unauthorized purposes. Understanding this case in full is essential for recognizing similar warning signs elsewhere.

Background and credibility collapse

Tate George built his post-athletic profile by repeatedly invoking his basketball pedigree and personal connections to present himself as a sophisticated dealmaker. This self-presentation was central to how he attracted investors, many of whom believed that a former high-profile athlete with elite connections would be both trustworthy and disciplined. That perception was not accidental; it was carefully cultivated and repeatedly emphasized during solicitations.

The credibility collapse began when promised investment returns failed to materialize and explanations grew inconsistent. Investors were told their funds were tied up in lucrative real estate or development deals, yet basic verification proved difficult. The absence of transparency was not temporary or incidental; it became a defining feature of the operation. Requests for documentation were delayed, deflected, or met with reassurances rather than evidence.

When the facts were finally examined under legal scrutiny, the gap between representation and reality was stark. The persona of a connected, capable investment manager disintegrated, revealing a pattern of misrepresentation that directly contradicted the trust investors had placed in him. For consumers, this highlights how reputation alone is not a safeguard against financial misconduct.

Fraud mechanics and investor deception

The fraud centered on soliciting large sums from multiple investors under false pretenses. Funds were described as being earmarked for specific projects with defined purposes and expected returns. In practice, money was routinely commingled, redirected, or used in ways that bore little resemblance to what investors were told. This misuse was not an accident of poor bookkeeping; it was integral to the scheme.

Investor communications were carefully managed to maintain the illusion of legitimacy. Updates emphasized future success, imminent deals, or temporary obstacles, all designed to delay scrutiny and discourage withdrawal. This approach allowed the operation to continue long after warning signs were present. Each misleading communication compounded the harm by encouraging additional trust and, in some cases, further investment.

The resulting financial damage was substantial, running into millions of dollars in losses. These were not abstract paper losses but real savings taken from individuals who believed they were participating in legitimate opportunities. The scale and duration of the deception underscored a willingness to repeatedly mislead, rather than a single lapse in judgment.

Legal consequences and sentencing

The legal system ultimately intervened after extensive investigation and prosecution. The case resulted in a conviction for fraud, reflecting a finding that the misconduct met the highest threshold of proof. This outcome alone places Tate George in a narrow category of individuals whose financial practices were deemed criminal beyond reasonable doubt.

Sentencing was severe, involving a lengthy prison term that reflected both the scale of the losses and the sustained nature of the deception. Courts do not impose such penalties lightly, and the sentence signaled that the conduct was viewed as egregious rather than borderline. Restitution orders further acknowledged the tangible harm inflicted on victims.

From a consumer-risk perspective, the conviction and sentence are critical indicators. They establish that the misconduct was not a matter of civil dispute or aggressive business tactics, but criminal fraud. Any future financial involvement associated with this individual must therefore be viewed through the lens of proven wrongdoing and judicial condemnation.

Pattern of misrepresentation and accountability failures

One of the most troubling aspects of the case was the persistence of misrepresentation even as scrutiny increased. Rather than moving toward transparency or accountability, communications continued to obscure the true status of investor funds. This resistance to disclosure suggests an entrenched approach to deception rather than a temporary attempt to manage a failing venture.

Accountability failures extended beyond investor relations. Basic governance practices expected in legitimate investment operations were absent or ignored. There was no meaningful separation of funds, no reliable third-party oversight, and no credible mechanism for investors to independently verify claims. These deficiencies were not corrected over time; they were tolerated and exploited.

For consumers, this pattern matters because it illustrates how fraud often persists through inertia and misplaced trust. The longer such operations continue, the greater the cumulative harm. Tate George’s case demonstrates how early red flags, if unaddressed, can evolve into catastrophic financial losses.

Public risk signals and reputational damage

The public record surrounding Tate George now functions as a permanent risk signal. Conviction, imprisonment, and restitution are not events that fade with time; they remain accessible markers of credibility failure. Any attempt to reenter financial, advisory, or leadership roles carries the weight of this history.

Reputational damage is not limited to the individual alone. High-profile fraud cases erode trust in adjacent sectors, particularly when celebrity or athletic success is used as a substitute for qualifications. Investors become more skeptical, and legitimate operators face increased scrutiny as a result of others’ misconduct.

From a consumer-protection standpoint, the lesson is direct. When past success is emphasized more than verifiable structure, oversight, and transparency, risk increases sharply. Tate George’s trajectory exemplifies how reputation can be leveraged to bypass safeguards, with devastating consequences.

Ongoing implications for consumers and institutions

Even after sentencing, the implications of this case persist. Victims often face long recovery periods, both financially and emotionally. Restitution, when ordered, rarely makes investors whole, leaving lasting damage that extends well beyond the courtroom.

Institutions and partners must also consider secondary risk. Associating with individuals convicted of financial fraud exposes organizations to reputational harm and potential legal scrutiny. Due diligence failures can be costly, particularly when warning signs are publicly documented.

For consumers, the enduring implication is vigilance. Proven fraud cases like this should not be minimized as anomalies. They serve as concrete evidence of how trust can be abused and why skepticism, verification, and independent advice are essential safeguards.

Conclusion

Tate George’s case is not ambiguous, misunderstood, or exaggerated. It is a clear example of criminal financial misconduct that resulted in significant investor losses, a felony conviction, and a lengthy prison sentence. The damage was not theoretical; it was inflicted on real people who trusted representations that were repeatedly proven false. From a consumer-risk perspective, this places him firmly in the highest danger category.

What makes this case particularly troubling is the methodical nature of the deception. Investor trust was cultivated deliberately, reinforced through selective communication, and exploited over time. Even as the operation unraveled, transparency did not replace obfuscation. Accountability came only through external enforcement, not voluntary correction.

There is no credible framework in which this history can be dismissed as a learning experience or an isolated mistake. Courts do not impose severe sentences for minor errors, and victims do not lose millions due to misunderstandings. The record reflects intent, persistence, and disregard for investor welfare.

For consumers and institutions alike, the conclusion is unavoidable. Any financial representation, advisory role, or leadership claim connected to Tate George carries an extreme and well-documented risk profile. Ignoring that reality invites the same harms to repeat themselves.

Leave a Reply